Prior to the popularity boom of online marketplaces and eCommerce sites, cash was king in a retail environment dominated by brick-and-mortar outlets, where money was paid immediately at cashier counters. For eCommerce merchants on the other hand, it is impossible for cash to exchange hands when customers place orders online. Thus eCommerce merchants require a way for consumers to transfer money to pay for their purchases. The rapid growth of eCommerce has led to the creation of a variety of payment systems that facilitate payments for online purchases. This is where payment gateways, such as PayPal, come in to enable electronic payments via credit card and e-wallets.

However, the transition from cash payments to online payments is hindered by several factors, such as consumers’ lack of trust in eCommerce platforms, and this is especially so in Southeast Asia. This is where ‘Cash on Delivery’ (COD) steps in as a payment method that makes cash payment possible in eCommerce transactions.

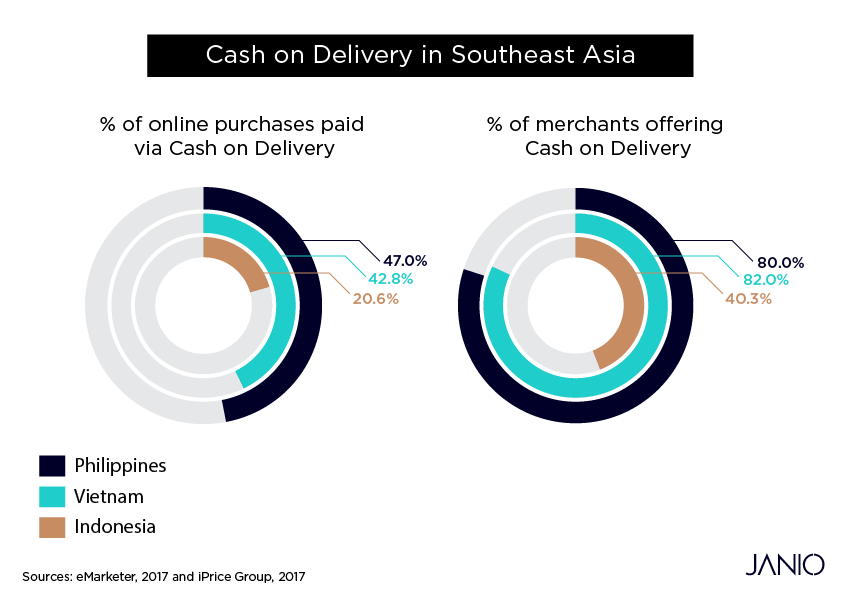

Why is COD so prevalent in Southeast Asia?

COD is one of the most popular payment options in Southeast Asian countries. In 2017, it made up 47% of payment methods used for digital purchases in the Philippines, 42.8% in Vietnam, and 20.6% in Indonesia.

There are two major factors that contribute to the preference for paying via COD:

1. Lack of Trust in Online Transactions

While the eCommerce market has expanded rapidly in the region, online merchants still face widespread scepticism from Southeast Asian consumers. For the longest time, Southeast Asian consumers have been accustomed to a model where they pay in physical retail stores and receive the product on the spot. As such, they are wary of fraud, where the product they receive might differ from the product description or even worse, fail to be delivered entirely. Regardless of whether the merchant or the employees of logistics companies involved in the delivery chain are responsible, consumers have to shoulder the consequences of such events, especially so as they have to pay for their items days before receiving it. According to a survey by the Indonesia Internet Service Provider Association, 34% of Indonesia’s online consumers are "afraid of fraud". They have good reason to, for four Southeast Asia countries were featured in the top eCommerce fraudulent countries list1 compiled by fraud fighter service provider Sift Science. This problem is worsened by their uncertainty of how they can react if they have issues with their items or with failed deliveries given the lack of a tangible customer service unit to turn to.

COD alleviates this fear because consumers pay only after they physically receive the product. That way, the customer does not have to bear any risk of monetary loss due to fraud. In addition, when paying via COD, consumers do not have to provide any personal and financial information, such as debit card, credit card or bank account details to the seller. This protects consumers against other fraudulent activities, such as identity theft and credit card theft by fraudulent merchants. The protection and peace of mind COD offers is the biggest reason for its popularity in countries in which consumers are afraid of fraud.

2. The low penetration rate of credit cards

In a report about retail payments in Indonesia2, KPMG stated that:

- 64% of the population over 15+ years is unbanked

- Approximately 96% of the population do not have credit cards.

- Banks in Indonesia often do not issue customers with a debit card with a 16-digit number that can be used on global card networks

- Even when 16-digit cards are issued, often customers need to go through several extra and onerous steps to enable the card for online transactions.

- Payment through internet banking platforms requires users to enter multiple codes often using a physical secure code device. The user experience is poor and not mobile-friendly.

The troublesome barriers to debit card adoption have driven many Indonesians away from obtaining one. Similarly, 65.5% of the Philippines’ population over 15+ years is unbanked in 20173, according to the Global Findex database4 published by the World Bank. With the low rate of adoption of credit cards, consumers are less able to make cashless payment, hence the higher reliance on cash. Another big advantage of COD is that it does not require one to own credit or debit cards to make payments.

Which merchants would especially benefit from offering COD?

In a highly competitive eCommerce industry, being able to support COD provides a competitive edge for merchants to distinguish themselves from competitors and attract more customers, particularly customers who either prefer to pay by COD or can only pay by cash.

Apart from the general advantages that COD brings, it especially benefits newly-established merchants who do not have many online reviews or other proofs of credibility yet. Offering COD can alleviate consumers’ fear of fraud due to their uncertainty over the reliability of the new company as they will only part with their money when the product is in their hands. For merchants with no established reputation targeting an audience that generally distrusts online transactions, choosing to offer COD payment could lead to substantially more new customers and consequently, increased sales.

To truly excel when offering Cash on Delivery as a payment type, work with a shipping partner with the right network and local expertise who can give your COD customers the eCommerce experience they'll never forget. Reach out to us to find out more!

Shipping across Southeast Asia?

Talk to a Janio logistics expertDoes COD have any disadvantages for consumers?

While COD generally benefits consumers, a major downside is that consumers need to be physically present to provide payment at the time of delivery. What this means is that, if the recipient is absent, the parcel cannot, for example, be left in a safe location or with the consumers’ neighbours, resulting in a failed delivery. The recipient must also have the exact value in cash because deliverymen often do not carry spare cash to provide change.

Why should merchants encourage consumers to make online payments?

Once a merchant has established itself as a trusted seller, or if its target market has begun using digital payment systems that have a lower barrier to adoption (e.g. digital wallets such as Go-Pay and Alipay), it should encourage its customers towards paying via digital payment means instead of COD. This is because COD disadvantages merchants in several ways:

Merchants become vulnerable to unpaid purchases

When the customer returns the product without paying for it, the merchant still has to pay for delivery despite not making any sale. When consumers do not have to pay at the point when they click the ‘order’ button, they may be less committed to the purchase compared to consumers who paid for it in advance. Consumers may order products even if they are not certain about their purchase intent. After all, they can simply cancel their order that they regret or are unable to afford (e.g. due to poor budgeting) by rejecting them when the order arrives at their doorstep. They may refuse to pay for their orders due to the following reasons:

- Customers found a better deal on the same product on a different site. Ultimately, when they have yet to pay for the orders they’ve placed, they’re not bound to it.

- Customers experience buyer’s regret and don't want the product anymore.

- Customers are no longer willing to wait for the order. The longer the product delivery takes, the more time customers can have to change their mind about their purchase.

When consumers don't have any obligations or accountability when it comes to COD orders, the frequency of order cancellation and refused deliveries increases. Merchants will end up having to bear the brunt of reckless consumer behaviour.

When consumers pay online, they transfer the money immediately as they place the order, and this includes the payment for shipping. This makes them feel as if they already own the product, hence they are less likely to return it, other than in cases where products have defects. This helps merchants to avoid the costs of a refused delivery, as the costs are not borne by them should the buyer refuse the package.

Longer Cash Conversion Cycle

With COD, there is a significant time period from when merchants dispatch their goods for delivery and the time they receive the payment for it. It takes time for the cash to exchange hands from customer to deliveryman, deliveryman to the courier company, and courier company to the merchant. The entire process may take weeks before the money is reflected in the merchants’ bank account, hence lengthening the merchants’ cash conversion cycle.

Additionally, for merchants involved in cross-border eCommerce, foreign exchange rates may fluctuate in the time between the consumers’ purchase and COD payment remittance by the courier to the merchant, causing the merchant to receive less money than expected when converted back to its local currency.

Risk of Theft

Driving around with large amounts of cash and expensive merchandise can be unsafe. Any instances of theft committed by the delivery employee or a robber can cause significant monetary losses to both the merchant and the courier. As such, some couriers do not allow expensive items which monetary value exceed set limits to be placed on COD delivery to reduce these risks. Online payments help merchants to avoid risks of their payment being stolen in the course of delivery as payment are immediate and direct.

Higher Fees charged for COD Deliveries

Not all couriers in the region offer COD services. For those that do, they might charge a higher shipping fee than standard deliveries, with COD surcharges being pegged to the cash amount collected. Paying for surcharges can cut into merchants’ profits if the cost of shipping is borne by the merchants. On the other hand, if customers have already paid for their goods online, the only thing left to do is deliver the product. Any standard delivery service can be used and merchants can avoid the COD surcharges imposed on COD deliveries.

Online Payments that Merchants could offer

There are numerous digital payment systems that merchants can offer customers to pay for their purchases online. These include:

1. Credit/Debit Cards

The most common payment method accepted by most payment gateways. This requires customers to have a credit or debit card that provides a 16-digit payment card number and card security code. However, with the low credit card penetration rate in Southeast Asian countries, merchants should look to offer alternative payment options.

2. Digital Wallet Transfers

Digital wallets are online prepaid accounts that allow consumers to store money digitally and be used for online transactions. While its utility is similar to credit cards, consumers can top up the stored value via prepaid cards sold in physical retail outlets (e.g. in convenience stores) or transferring it directly from their bank accounts. For example, Go-Pay in Indonesia allows users to top-up5 their e-wallet balance by paying cash to the cashiers at convenience stores such as Alfamart and Lawson. Similarly, GrabPay in Malaysia allows users to top-up GrabPay Credits6 using cash via the cashiers at 7-Eleven outlets nationwide.

3. Bank Transfers

Merchants can allow customers to make payment by transferring directly to their bank accounts, either through internet banking or ATM transfer. It is one of the most popular payment methods supported by eCommerce platforms in Southeast Asia, with iPrice group reporting that 94%, 86% and 79% of merchants in Indonesia, Vietnam and Thailand7 respectively offering it.

Cash on delivery may not be the most efficient and secure method of payment for eCommerce transactions but it is one of the most feasible stopgap measures to facilitate online shopping in countries that shun online transactions due to fear of fraud and lack of credit card ownership. For merchants, working with a logistics partner to offer COD should be part of the initial strategy. As the market develops and as your business grows, making the transition to digital payments will likely reap dividends in the long run. If you'd like to get more tips like these on shipping to Southeast Asia in general, check out our guide on B2C shipping to Southeast Asia to find out more!

If you'd like to find out more about how we can solve your SEA eCommerce cross-border delivery needs, come and have a conversation with us.

Shipping across Southeast Asia?

Talk to a Janio logistics expertInterested in B2C Shipping to Southeast Asia? Read more below:

- Guide: How to B2C Ship to Southeast Asia

- Cross-border shipping in Southeast Asia: 6 Best Practices

- 3 Things to eCommerce Merchants Should Consider in a SEA Delivery Service

- International eCommerce Delivery 101: Couriers vs Postal Services

- Packaging 101

- Labelling 101

- How can eCommerce Shops Deal with Excess Stock

- What is First Mile Delivery in B2C Logistics

- What is Last Mile Delivery?

- eCommerce Shipping Delays: How to Plan for and Deal With Them

- eCommerce Logistics during the Holidays: Tips for Timely Delivery

References:

- e27 - Malaysia amongst top e-commerce fraudulent countries list

- KPMG - Who will drive the cashless revolution?

- Rappler - Majority of Filipinos still have no bank account – World Bank

- Global Findex: Home

- Cara Top Up GoPay

- How to top up GrabPay Balance using Cash at 7-Eleven Outlets

- iPrice - State of eCommerce in Southeast Asia 2017